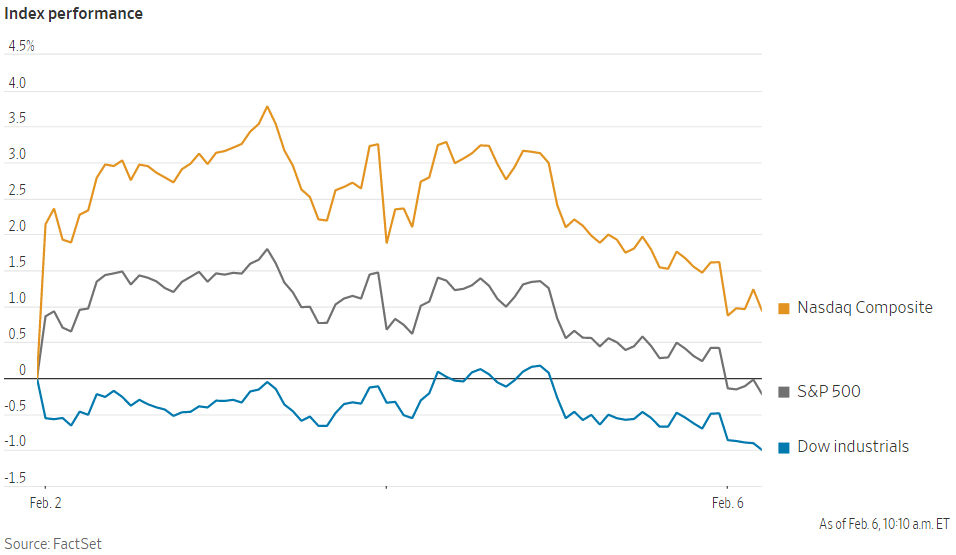

US Stocks Open Lower, Treasury Yields Rise

Stocks ripped higher at the start of 2023, boosted by wagers that slowing inflation will encourage the Fed to pause rate increases, then unwind some later this year. But Friday’s surprisingly strong jobs report suggested the Fed might need to keep raising rates to curb wage growth and hold rates steady for an extended period, investors said.

“What seems to have driven markets this year seems to be expectations of either fewer rate hikes or, after the peak in rates, some fairly significant rate cuts, as well as perhaps some more optimism over global growth, particularly in Europe and China,” said Edward Smith, co-chief investment officer at Rathbones.

“The selloff in the last couple of days might be some realization, particularly on the rates side of things, that the markets got carried away,” he said. Given how rapidly prices have risen, Mr. Smith added, “We’ve got a long way to go. That’s going to keep the Fed from delivering those rate cuts.”

Fed Chairman Jerome Powell is due to give an interview Tuesday. Investors will trawl his remarks for clues about the central bank’s response to the job numbers.

See what’s on the Economist 2022 today by signing up, you will enjoy savings of up to 70%

The focus will be on whether Mr. Powell emphasizes the central bank’s view that short-term rates will peak at more than 5%, said Jim Reid, a strategist at Deutsche Bank, compared with the current range of 4.5% to 4.75%.

According to CME Group, traders in interest-rate futures see a three-in-five chance that the Fed’s target will still be at 5% or above by late September, up from less than a one-in-two chance a week ago.

Up ahead is another busy week for US corporate earnings. Gaming companies Activision Blizzard and Take-Two Interactive Software are due to report after Monday’s close, as is Pinterest. The private-equity groups KKR, Carlyle Group, and Apollo Global Management are scheduled to file results in the coming days, as are others such as Disney, DuPont, PepsiCo, and Uber Technologies.

Over half of the S&P 500 have filed earnings for the final quarter of 2022. Around 70% have beaten analyst forecasts for earnings per share, according to FactSet. But companies routinely beat such predictions, and Mr. Smith at Rathbones said that is one of the lowest rates of the past decade—a shift he said is consistent with a looming recession.

Get Barron’s news subscription unlimited access to daily news

A flurry of news related to mergers and acquisitions drove stock moves in morning trading. Newmont fell 4.9% after the gold mining company made a roughly $17 billion offer for Australia’s Newcrest Mining. Public Storage dropped 2.3% after saying it had made an $11 billion unsolicited offer for Life Storage. And shares in Catalent rose 24% after Bloomberg News reported that Danaher had expressed interest in taking over the contract manufacturer.

Oil prices rose a day after the West hit Russian refined fuels such as diesel with sanctions on commodities. Front-month contracts for Brent crude added 0.8% to $80.58 a barrel. Brent is trading in line with where it was when an earlier round of sanctions took effect on Dec. 5, easing concerns that the restrictions will lead to higher global energy prices.

Overseas markets broadly fell. The Stoxx Europe 600 lost 0.8%, led lower by technology and real-estate stocks. China’s Shanghai Composite Index lost 0.8%.

Japan was an outlier. The Nikkei 225 rose 0.7%, and the yen weakened against the dollar after a report that Bank of Japan official Masayoshi Amamiya had been approached to succeed BOJ Gov. Haruhiko Kuroda. Analysts said Mr. Amamiya is the most likely of the leading candidates to continue with Mr. Kuroda’s easy monetary policies.